How does your company stack up against best-practices and costs of card based sales? Payments analytics provides clarity, understanding, and helps reduce fees more easily and faster. Like anything, if you can’t measure it, you cannot improve it.

You likely have heard that the merchant card market in the United States is considerably more complex than most other nations in the world. Did you know the credit interchange rates in the U.S. are the highest in the developed world? This might raise the question as to how your company stacks up against best practices and overall costs of acquiring these sales given the continued strong growth of card based sales.

First, what makes card payments so complex? There are numerous players who touch every transaction. There are the Consumers who purchase the goods with their debit and credit cards. There are the issuers of the cards, the merchants who accept the cards, and about dozen different potential players in between!

Some intermediaries play more than one role. There are the closed network providers, eWallets, eWallet platforms, merchant processors, gateways, mobile POS providers, merchant acquirers, 3rd party processors, point of sale terminal vendors, integrated system providers, Independent Sales Organizations (ISO’s), on-line providers, in-store providers, fraud control providers, customer authentication providers, card associations, and others!

So, I think we can agree that it is a complex matrix of players between the swipe of the card and the deposit of funds into the merchant’s bank account. But where do the fees get applied, who gets paid to do what, and how do they get paid?

The overall cost per transaction is a percentage of the value of the transaction and ranges typically from 1.5 to 3.5% of the purchase. This total cost is referred to as the “effective cost” and is deducted by the acquirer from the total transaction before the merchant gets its net credit in its bank account upon settlement. There are three primary components to effective cost: 1. The interchange fee paid to card issuers; 2. dues and assessments paid to major card networks (e.g. Visa, MasterCard, Discover); and 3. acquirer fees paid to the merchant’s bank or payment processor.

First, the interchange fees typically account for 85% to 90% of the fees applied to a transaction, and are set by the different card networks. In the U.S., there are over 700 different interchange rates that could apply to a specific card transaction. The interchange fee depends on many factors, including the type of card, the merchant’s industry code, the amount of the transaction, whether the card is present at point of sale or if the transaction is done through a website (card not present). The interchange revenue received by the issuers covers costs of any rewards programs, their internal costs, including fraud costs, leaving the remainder as profit. Despite the complexity, interchange fees CAN be managed and in some instances, negotiated with the card networks.

Next is network assessments and dues. For a merchant with greater than $100 million in card sales, these fees would account for about 8% of the total merchant discount fees. Lastly, the Acquirer fees account for only 2% of the total merchant discount fees. So, the interchange fee is by far the largest component.

For an example, say a merchant completes a $200 sale and that merchant’s effective cost is 2.50%. On average, the cost of interchange is $4.25, the cost of assessments and dues is $0.65 and the cost of processor services is $0.10. The merchant is funded $195.00, less $5.00 from fees above.

Most merchants do not understand the rationale for so many interchange rates. Visa/MasterCard/Discover have set up a complex matrix of over 700 possible interchange rates in the United States. This complexity is due to macro and micro forces: macro forces at the market level and micro forces at the individual merchant level. From a market perspective, card networks compete with each other to sign up banks/issuers by promising higher interchange revenue. Card Networks also create new interchange categories to increase card sales from emerging markets like insurance payments, rent payments, small ticket payments, etc. And the Durbin Amendment in 2011 also created a new set of regulated interchange categories. From a micro, or individual merchant perspective, there are different interchange categories based merchant’s Merchant Category Code (MCC), the type of cards accepted (i.e. Visa Traditional, Visa Rewards, Visa Signature, Visa Debit, etc.), swiped vs keyed, and a merchant’s adherence to compliance standards.

So, what can a merchant do to make sure they are achieving optimal interchange rates?

First, verify with your merchant acquiring bank that your MCC is correctly assigned.

Next, merchants should employ tools to actively monitor their interchange costs on a monthly basis and be able to easily investigate the sources of significant variances and take action (e.g. streamline authorization and settlement systems).

What, if anything, is the merchant doing with its merchant statements? Are there increasing numbers of transactions that do not qualify for the best rates? Are these downgrades being analyzed for root causes? The top reasons for downgrades include 1. Delayed settlement or stale authorizations; 2. No AVS (Address Verification System) for Key Entered or Card Not Present (CNP) Visa cards; 3. No Level 2 or Level 3 data for Commercial Cards; and 4. Mismatch of Authorized and Settlement amounts (e.g. split shipments for ecommerce merchants).

Is the merchant optimizing Point of Sale and payment systems for AVS prompts? PIN prompting or least-cost routing? Level 2/3 data transmission for commercial cards?

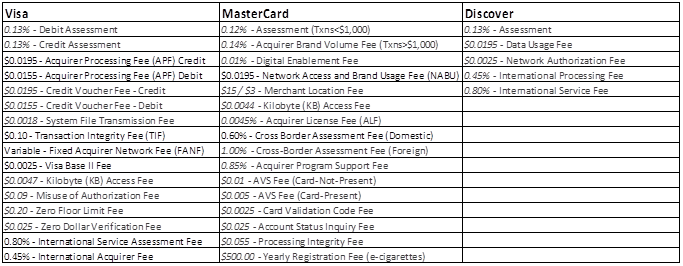

Although the Assessments and Dues portion of the merchant discount cost is significantly less than Interchange fees, these fees still account for an average of 0.17% of gross sales. And the effective cost of these fees has increased over the last decade by 55%! There exists some complexity as there are over 30 unique fees assessed by the 3 card networks based on different transaction characteristics:

Can any of these dues be ‘optimized’? Some can. For example, if you ensure that every authorization is either settled or reversed, you can reduce Transaction Integrity Fees, misuse of Authorization Fees, and Processing Integrity Fees.

The last component of the merchant fees is acquiring fees. They are certainly the smallest cost component but often get the most attention since they are easiest to analyze. From your acquiring relationship, some best-practices to consider include: 1. Request interchange pass-through pricing. 2. Consolidate as much of your U.S. volume with a single acquirer. 3. If you anticipate your card volume will increase, build fee tiers into a contract so that as transaction volume grows, the acquiring fees automatically decrease.

As there likely is very high visibility and importance given to the effectiveness of your merchant acquirer relationship(s), you will want to schedule regular reviews (quarterly or semi-annually at the least). At these reviews, request the acquirer’s view of processing effectiveness, gain industry and regulatory updates, receive helpful industry segment best-practices to improve processing and reduce risk of fraud, and lower acceptance costs. Be sure to be transparent in communicating any expected changes in your sales volumes, challenges you are experiencing, and any new initiatives planned. If your acquirer or the card networks sponsor any industry round-tables, seek out and participate to remain current on all that might impact your business performance.

If your activity level warrants a closer look at your card payments, you may need tools to assist you in performing a detailed analysis. Using payment analytics tools can provide powerful insights and clear justification for taking certain actions that can rapidly help improve effectiveness and reduce interchange and acquiring costs. Like anything, if you can’t measure it, you likely cannot improve it.

So how to you build such a tool? For all payment types, you CAN build a repeatable, sustainable payment analytics program. You should follow these 5 steps:

Step 1: Identify desired key metrics or performance indicators for each payment type.

Step 2: Gather data from your merchant and bank statements over each desired period (monthly, quarterly, etc.)

Step 3: Input and organize the data in Excel or another database

Step 4: Segment the details of the card interchange data into relational tables

Step 5: Analyze the data on a regular basis to determine trends and actionable items.

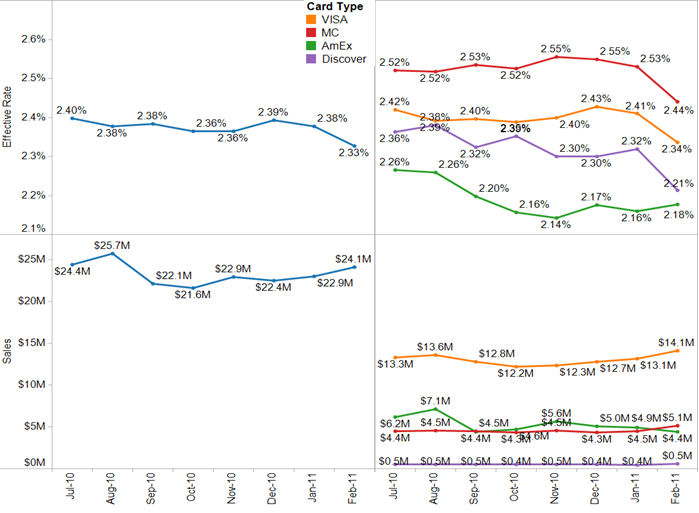

Here is a sample graph of 8 months of sales (July to February) showing overall ‘Effective Interchange Rate’ and then broken down into payment tender costs as well.

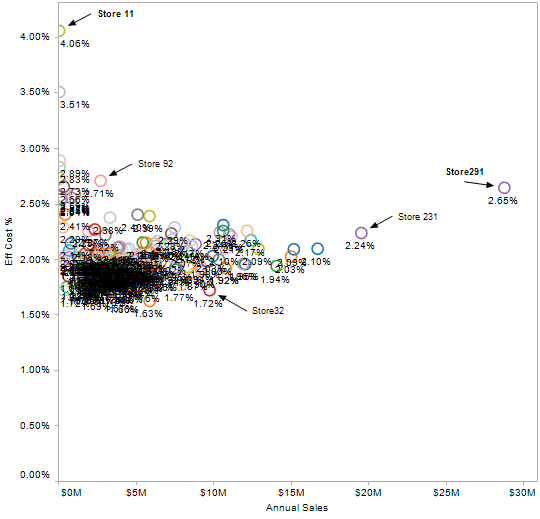

Another analytics view maps MIDs (e.g. store locations) against card sales and effective cost. This cluster-plot chart quickly highlights locations that have a high effective cost and require further action. For example, there may be opportunities to duplicate best-practices at lower effective cost MIDs or business units to those less efficient, high cost MIDs or business units.

Or perhaps you are interested in tracking the level of transaction downgrades and want to identify areas for improvement.

![]()

In conclusion, due to the complexity and high cost of interchange fees in the U.S., there is a critical need to focus on and optimize what may be a merchant’s highest expense in actualizing revenue. Payments analytics can make the task of understanding and reducing card fees easier and faster. Large retailers have created payments teams that focus on and optimize card fees. Who is optimizing card fees at your company?