/new-website-headshots/laura-194x221-newde938f39-ed18-4a87-a939-58943c00f407.png?sfvrsn=cfeaa4ba_14)

The U.S. market offers a wide variety of competitive alternative networks to which merchants can route debit transactions that can deliver a reduced cost of payment acceptance. Yet there are barriers in the market. What is the opportunity and the considerations?

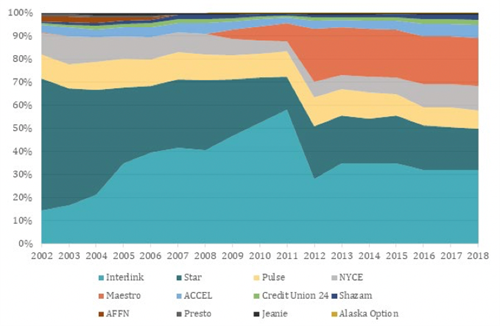

The debit market in the U.S. is represented by at least twelve competing networks. The estimated market shares of these networks reflect that since Durbin the competition among the networks has increased (Figure 1).

Figure 1 – Source: CMSpi

Let’s say an average retail site has $1 million in sales of which 30% of those sales are card-based. Assuming 40% of those card sales are debit and a potential cost savings target of 25 basis points, smart routing of debit transactions among competitive networks could result in $300 in savings per location. At 500 U.S. locations there is $150,000 in potential cost savings on the table.

There is real meat on the bones of opportunity here. I encourage you to educate yourself on the steps to optimize your routing alternatives. Our merchant-only polling at Annual Conference 2018 showed that almost 3/4 of our members in attendance called out operational efficiencies/cost reduction as one of their top initiatives planned for 2019. Although that same polling showed that 19% of the members present had already implemented smart routing to reduce their cost of acceptance and another 56% had implemented both smart routing and some form of incentive program, that suggests there are many others that have not.

In addition to cost management, there are additional benefits to competitive routing such as selective network routing based on performance including transaction speed, approval rates, and unplanned outages. Have you considered smart routing as part of your payment strategy; and, if so, how far along are you on execution?

We know several hurdles remain in the ability for merchants to get full access to competitive routing in the U.S. market. One hurdle is limitations in PINless support of issuers despite the fact the majority of domestic debit networks have introduced PINless as a competitive offering to “no signature” global network programs. PINless enables a frictionless experience at the physical point of sale for most merchant verticals (petro may be one primary exception to call out) with comparable risk to the merchant as compared to the “no signature” global programs. Unfortunately, some issuers have opted out of enabling PINless on their portfolios, and that participation rate does not seem to be improving.

Another challenge is in the remote commerce channels. The approach some global networks are taking on the implementation of payment network tokenization is that a merchant must choose payment tokenization, a product which suggests enhanced security in that the merchant eliminates the PAN from its environment, and sacrifice routing choice. Some global networks are taking a softer approach in that a merchant can choose both payment tokenization and alternative routing on debit transactions; however, some of the features that payment tokenization offers such as cryptogram validation and domain control restrictions will not be provided which does disadvantage the alternative network and its issuer in making an informed approval decision.

Although alternative routing of EMV contactless transactions is possible, it does require considerations in the software of the terminal which can increase the cost of implementation (development and certification) for the point of sale. In addition, the biometric authentication method often referred to as CDCVM (consumer device cardholder verification method) or ODCVM (on-device CVM) is not available to the Common AID which essentially means debit transactions routed to alternative networks will not be fully informed that a transaction was authenticated on the mobile device with a fingerprint or other biometric authentication. Again, this approach disadvantages the alternative network and its issuer in making an informed approval decision.

Similar in nature to the issues with biometric authentication, ODA (offline data authentication), which is most relevant for U.S. transit, is not available to the Common AID for some networks which limits transit from competitive routing alternatives given the nature of their operational environment requiring speed and dependency on offline authentication capabilities.

MAG recently launched our newest Community of Practice (COP) on Debit Routing which is in the planning stages of how to approach these challenges in the U.S. in order to gain positive momentum in the best interest of our members. Please contact Laura Townsend if you have a passion on this topic and availability to dedicate some time to participate in our bi-weekly calls and efforts in between.

In summary, expanding your debit routing means freedom by creating competition and choice in the market, loosening the stranglehold legacy providers have had. The benefits:

Choice

Makes networks compete for your transactions and gives greater control of routing decisions

Improved Profits

Increase net profits with reduced payment acceptance costs

Customer Experience

Comparable checkout experience for your guests

The call to action for merchants to get started: Do Something!

- Leverage your Acquirer

- Educate Yourself. Stay Informed. Advocate.

- Evaluate Scope of the Opportunity

- Engage Domestic Debit Networks

- Identify the ROI

- Implement

- Maintain & Refine