So, what makes Europe different from the rest of the world?

Much more regulation

In comparison to other regions, Europe is quite uniquely organised. The European Union and the wider European Economic Area are complex due to the multi-cultural mix of member states. The law-making process is lengthy and somewhat convoluted, with the European Commission taking most of the initiative, for example, in the 24 September 2020 Retail Payments Strategy. After such an initiative leads to legislative proposals, the European Parliament and European Council discuss and reach consensus about possible amendments. Only at that point will directives and regulations become final with member states required to implement (‘transpose’) these elements into national legislation within a specific timeframe. During the entire process, external interest groups are invited to submit their views but may also send in unsolicited positions, hoping to influence lawmaking to suit their constituencies.

At the last count, over 20 different pieces of European legislation seek to regulate payments. These range from pure payments services to data privacy, accessibility, AML, consumer credit, and European Identity, to name a few. The complex interplay of these regulatory requirements makes life for merchants increasingly difficult and we continue calling upon the legislators to ensure greater coherence, harmonisation, and operability by reducing the burden and cost of regulation for merchants.

Non-bank payment licences

Another European peculiarity is that non-banks can obtain payment licenses. Where credit institutions (banks) can also offer loans and mortgages alongside holding money and performing transactions. E-money institutions cannot give credit but can hold money on customer accounts. Payments institutions, like Payment Initiation Service Providers (PISPs) and Account Information Service Providers (AISPs), cannot give credit or hold money, but they can respectively execute a payment transaction or obtain data from an account, such as transactions, addresses, and account holder details. Towards the end of 2022, approximately 200 of these third-party providers (PISPs and AISPs) were present in Europe.

This ‘unbundling’ is intended to promote competition and innovation, but on the flipside, it can lead to fragmentation and supervisory headaches. Indeed, since all participants throughout the ecosystem need to make a living in the end, this development perversely can lead to rising costs of payments for merchants.

Importance of domestic schemes

Debit schemes such as girocard in Germany, Bancomat in Italy, Cartes Bancaires in France, and Multibanco in Portugal are thriving domestically. Although their acceptance is limited to one country, with non-domestic transactions using Mastercard or Visa rails, these ‘co-badged’ cards are important to merchants who appreciate their attractive fees and the competitive edge they represent with respect to global schemes. Increasingly, however, domestic schemes are under threat, with issuers opting for mono-badged Debit Mastercard or Visa Debit cards, which are Interchange++ priced, instead of the usually fee-per-transaction-based domestic schemes.

And what are the hot topics for Europe in the (near) future?

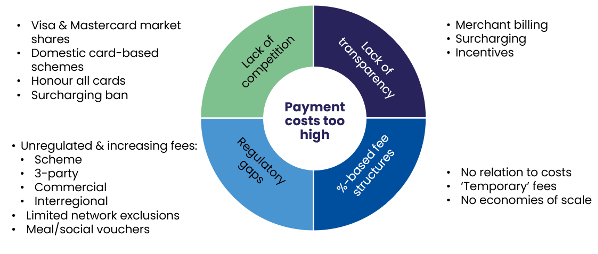

Rising payment costs are a huge concern

With the rise of Alternative Payment Methods (APMs) like Buy Now Pay Later (BNPL), the average cost of payments is increasing. Even though consumer interchange is capped by regulation in Europe, all non-regulated scheme fees and commercial and interregional interchanges have increased so much that these have minimised the overall benefits of the regulation. Overly expensive payments costs are caused by four groups of issues:

Merchants continue to push for solutions in these four areas and the European Commission is undertaking a review of card payment fees with a report on this due by the end 2023.

Investigation phase of the digital euro

In 2021, the European Central Bank (ECB) launched an investigation into a Central Bank Digital Currency (CBDC) for the euro area. With much preparatory work already undertaken, as shown in the most recent progress report, a go/no-go decision is now expected towards the end of 2023. EuroCommerce has compiled an Info paper for members and the public titled: “Digital euro – why should retailers and wholesalers care?,” which includes a useful comparison of CBDCs with other payment methods.

As reflected in our recent position paper, in general, merchants should welcome the digital euro as a more cost-effective alternative to most other current payment methods. However, there are concerns about consumer uptake in the absence of a compelling reason to use the digital euro. With free basic use for consumers and potentially mandatory acceptance, merchants are exposed to Payment Service Providers (PSPs) overcharging for digital euro services and the ECB has indicated that this issue must be addressed by legislators.

Results of PSD2 Review upcoming Instant Payment Regulation (IPR)

The end of June 2023 will see the publication of legislative proposals from the European Commission on ‘payment services,’ following the review of the Second Payment Services Directive (PSD2). Together with proposals around Open Finance and enabling the digital euro, this ‘PSD3’ will set the agenda for EU payments over the coming five to seven years and should provide clarity on how the EU Retail Payments Strategy has been put into action.

Later in the year, the Instant Payment Regulation will come into force obliging banks to offer instant credit transfers, and to do so at no additional cost compared to ordinary credit transfers. In addition, checks must be built-in, including an account name check for customer protection and a check against Anti Money Laundering (AML) and terrorist financing blacklists.

Merchants hope that IPR at Point of Interaction (POI) will bring some of the long-awaited competition that has long been absent with regard to the dominant card schemes. They are keen to have both QR- and NFC-based initiation of transactions available on any type of mobile device.

SEPA Payment Account Access scheme (SPAA)

This voluntary scheme intends to standardise the APIs used between banks and PSPs for both transaction and account data. It should mitigate the complexity, lack of availability, and lack of performance of the free APIs that banks were forced to make available after PSD2. In addition to offering premium services, the scheme strives to find the right distribution of risk and value. As merchants, we are cautiously optimistic and engaged in the discussion, whilst we have yet to see how SPAA might improve customer experience and cost to the merchant.

epi Company – European Payments Initiative

Last but not least, after months of radio silence, EPI Company has announced the acquisition of Payconiq International and iDeal, in addition to further banks from Belgium and The Netherlands as shareholders alongside key German, French, Belgian, and Dutch banks that already wanted to commit.

This is interesting, for the following reasons:

- after epi had to drop the idea of issuing their own card-based solution, they instead opted for a digital payment solution based on Instant Payments. See above under IPR.

- Payconiq International provides the technology for iDeal in The Netherlands and incorporates an additional company operating Payconiq as a payments solution in Belgium and Luxembourg proving this system's operability.

- It seems that finding a single European solution that ‘runs’ on Instant Payments at POI and which can also support a digital euro and a European identity is now one big step closer.

What is EuroCommerce’s involvement?

Together with merchant organisations from aviation, hospitality, and eCommerce, we have set up a Merchant Payments Coalition, exchanging information and agreeing on common positions to provide a clearer and more coordinated voice from the payment acceptance side.

EuroCommerce’s members are participating in many different private and public initiatives ranging from expert groups and standardisation bodies to co-leading multi-stakeholder teams, in order to further develop and manage payment schemes.

Increasingly big merchants in Europe set up in-house PSPs, with either payment or e-money licenses. In part, this is intended to manage the very important payments section the customer's personal retail and wholesale experience, but is also aimed at controlling costs and making better use of payments data.

For more information, contact Atze Faas on faas@eurocommerce.eu.

About the Author

Atze Faas (LinkedIn), is payments adviser at EuroCommerce and independent payments speaker and consultant. Atze has a degree in Business Economics, has worked 30+ years for bp, is Dutch, plays golf, and speaks several languages.

EuroCommerce is the principal trade association for the retail and wholesale sector in Europe, representing leading global players as well as millions of small businesses. The sector generates 10 percent of European GDP, some 250m transactions per day and one in seven jobs. EuroCommerce continues to be recognised as a strong voice on European payments from the merchant's perspective.